Financing a Tiny Home or ADU With a Tiny Home Loan

From Tiny House Dreams to Big Reality!

Whether you’re drawn to a minimalist lifestyle, environmental sustainability, or the idea of owning a home without a huge mortgage payment, financing your tiny home can seem like a daunting task. Many aspiring tiny homeowners worry that they won’t qualify for a tiny home loan or that their project isn’t financeable. However, there are more options for tiny home loans and ADUs than you might think and we’re here to share those resources with you!

One of the most common questions people ask when exploring tiny homes or ADUs is simple: “How do you finance one?” The answer depends on a few important factors — especially what type of home you’re buying and whether it will be permanently attached to land. Understanding this early in the process can save a lot of time, frustration, and unexpected costs later.

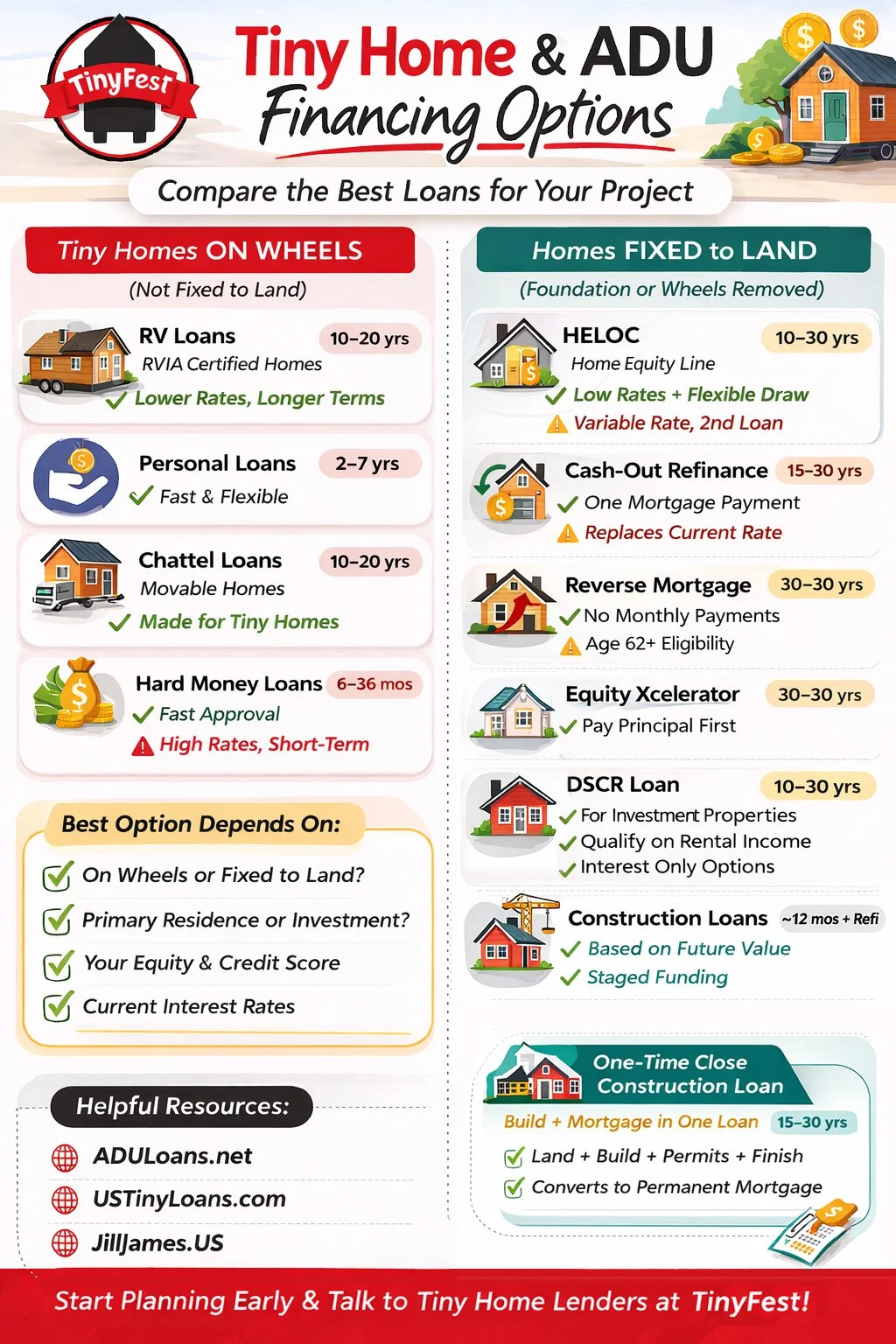

In general, for lenders, tiny homes and small dwellings fall into two broad categories:

• Homes on wheels (not fixed to land)

• Homes permanently attached to land (foundation or wheels removed)

The category your home falls into determines which financing options are available.

Tiny Homes on Wheels - Not Fixed to the Land

Tiny homes on wheels offer flexibility and mobility, but they require a bit more strategy when it comes to financing. Without proper planning, a beautiful tiny home can quickly become a logistical and financial challenge.

Because these homes are not permanently attached to land, most lenders do not classify them as real estate. That means traditional home mortgages typically are not available, even if the home will be used as a primary residence or placed in a backyard. Instead, financing options generally fall into the personal property category.

Common Financing Options for Tiny Homes on Wheels

RV Loans: If the tiny home is RVIA certified, some lenders will treat it similarly to a recreational vehicle. Utilize this recommendation at your discretion. RV Loans are typically not approved if customers are using the RV as a primary residence. Therefore, if you’d like to finance your RV and use it as a tiny home full-time, you would need to secure financing while you have a traditional full-time residence. In this situation, you would finance the RV as a recreational vehicle for use camping on the weekends and then once your loan in secured, you could sell your home or move out of your apartment.

Pros: Lower interest rates than personal loans. Longer loan terms. Designed specifically for mobile units.

Cons: Requires RV certification. Not all tiny homes qualify.

Personal Loans: Personal loans are unsecured loans that can be used for almost any purpose.

Pros: Very fast approval process. Flexible use of funds. No property requirements.

Cons: Higher interest rates. Shorter repayment terms.

Hard Money Loans: Hard money lenders provide short-term financing based on asset value rather than credit. These are usually used as temporary financing until another solution is arranged.

Pros: Faster approval. Flexible qualification requirements.

Cons: Higher interest rates. Short repayment timelines.

Chattel Loans: A chattel loan is a specialized loan designed to finance movable personal property. Instead of being secured by land like a traditional mortgage, the loan is secured only by the home itself.

Pros: Faster approval. More flexible financing for movable homes. Specifically designed for structures like manufactured homes or tiny homes

Cons: Higher interest rates. Larger down payments. Shorter loan terms

Park Model Homes: A Special Category: Park model homes are a type of tiny home built to RV standards but designed for more permanent placement. Because of this hybrid classification, they may qualify for additional financing options. Some specialized lenders offer financing programs specifically designed for park model homes. These lenders understand the structure, zoning, and placement challenges that often come with these homes.

FHA Title I Loans -These government-backed loans can be used to finance a park model home even if you do not own the land.

Pros: Government backed. Lower down payments. Flexible credit requirements

Tiny Homes Fixed to the Land - As an ADU

When a tiny home or ADU is permanently attached to land — either on a foundation or with wheels removed — lenders usually classify it as real estate. This opens the door to many more traditional financing options. These homes can sometimes be financed similarly to a home addition, renovation, or new construction project.

ADUs, also known as Accessory Dwelling Units, are an increasingly popular type of structure for backyard studios, granny flats, and offices. Meredith Munger at Cross Country Mortgage and ADUloans.net and Jill James at NEXA Lending and JillJames.us are experts on ADU financing and can provide you with several options to consider. They are leaders in ADU loans and keep us updated on changes within the financial world that apply to ADU and tiny home loans. For example, in 2025, OTC Construction DSCR loans (Fix/Build and Hold) became available.

Using Equity from Your Home

If you already own a home, one of the simplest ways to finance an ADU or backyard tiny home is to use the equity you already have.

HELOC (Home Equity Line of Credit): A HELOC allows homeowners to borrow against the equity in their home. Most lenders allow borrowing up to about 80% of the home's value (loan-to-value).

Pros: Usually one of the lowest interest rate options. Flexible borrowing. Interest paid only on the amount used. Funds can be used gradually as construction progresses

Cons: Variable interest rates tied to the prime rate. Creates a second loan payment. Based on current home value, not the value after adding the ADU

Cash-Out Refinance: A cash-out refinance replaces your current mortgage with a new larger loan, allowing you to take out the difference in cash. For homeowners with extremely low mortgage rates, refinancing may not always be the most attractive option.

Pros: Single monthly mortgage payment. Can refinance the entire home value Provides full funding upfront

Cons: Based on current home value. Payments apply to the entire borrowed amount Current mortgage rate may be lower than today’s rates.

Reverse Mortgages: First-Lien Reverse Mortgages are a specialized loan designed for homeowners who meet specific age requirements, typically starting at 62, with some available to those 55+. The loan is secured by your primary residence. It is used to pay off existing mortgage debt and provides access to home equity that can be used for any financial purpose.

Pros: No required monthly P&I payment. Continued ownership.

Cons: Age requirements. Slightly higher interest rate.

Equity Xcelerator: First-Lien HELOC to purchase or to cash out equity from a primary, secondary, and investment property. Structured as a “pay principal first” loan with sweep bank account connection enabling quicker loan payoff and significantly lower interest paid.

Pros: Pay principal first. Lower overall interest paid.*Longer access to equity.

Cons: Tighter Debt-to-Income (DTI) requirements.

Using Equity from Your Investment Properties

Debt Service Coverage Ratio (DSCR) Loans: First-lien and second-lien loans for investment properties to purchase or to cash out from investment property equity. Qualify based on rents, expenses, and credit score. No personal income documents needed.

Pros: Qualify on rents income. Low interest rates. Interest only available.

Cons: Investment properties only. No Owner-occupied.

Construction Loans & Renovation Loans (First Lien Position)

Construction /Renovation loans: These loans are designed specifically for building or major renovations. Instead of receiving the money all at once, funds are released in stages (called draws) as the project progresses.

Pros: Based on the future value of the home after the ADU is completed. Interest-only payments during construction. Structured for building projects

Cons: Requires a licensed and bonded contractor. More structured timelines. Usually short-term loans (often around 12 months). Typically refinanced into a permanent mortgage after completion

Popular Construction Loan Programs - Some pros of these loans include: Lower credit score requirements, higher debt-to-income flexibility, lower down payments.

Fannie Mae HomeStyle Loan

A flexible renovation loan backed by Fannie Mae. If used when purchasing a home, buyers can finance up to 97% of the future value of the property. If adding an ADU to a home you already own, you may be able to borrow up to about 90% loan-to-value.

FHA 203(k) Loans

FHA renovation loans allow homeowners to finance renovations and construction with more flexible qualification requirements. Two common versions include FHA 203K and FHA 203KS (Streamlined)

Freddie Mac Home Possible & CHOICE Renovation

A lower cost, single close loans used for purchasing & renovating/expanding (adding an ADU) a home. Or, for renovating & expanding your current primary, second, or investment property. Higher Loan-to-Value is allowed. Estimated income from ADU can be used to qualify for the loan.

OTC Construction Debt Service Coverage Ratio (DSCR)

OTC construction loan is used for investment properties. It uses “future rents” to qualify, not your personal income or tax returns. Multi-unit homes are allowed (1-4). Owner-built projects are eligible. There is a minimum down payment of 25%.

Other Government Options

Depending on eligibility, some borrowers may also qualify for a USDA loan or a VA loan. These can sometimes be used for construction or renovation projects involving ADUs.

ADU Construction Loans (Second Lien Position): Another option designed specifically for ADUs is a construction loan in second lien position. This type of loan does not refinance your existing mortgage and adds a second loan based on the future value of the home after the ADU is built. This can be an attractive option for homeowners who currently have very low mortgage interest rates and do not want to refinance their primary loan.

Tiny Homes Fixed to the Land - As a primary residence

Financing a tiny home as your primary residence is absolutely possible,

but it usually depends on a few important factors that lenders will evaluate

These include things like:

- The size of the home.

- Whether it meets local building codes.

- How the structure is classified by the county or state.

- Whether you own the land where the home will be placed.

Chattel loans, personal loans and RV may be your best options. However, depending on the variables, you may also qualify for traditional real estate financing, such as construction loans, renovation loans or construction-to-permanent loans.

Because there are so many variables involved, this is usually a one-on-one conversation with a lender who understands tiny homes and small dwellings. Working with a knowledgeable lender who has access to a wide network of loan programs and investors can help you indentify financing paths that many traditional banks may not offer.

Tiny Home Builder Financing

Some tiny home builders and manufacturers have established relationships with lenders for financing and can be incredibly helpful as you seek financing for your tiny home. Or, they can likely recommend financial institutions that have provided tiny home financing for their previous customers. For example, Clever Tiny Homes helps facilitate a relationship between their customers and lenders, such as US Tiny Loans, who are experienced in financing ADUs.

Get Creative!

Tiny home financing will require some creativity and persistence. If you have a good relationship with your local bank, consider a personal loan or construction loan to finance your tiny house project. If you are a landowner, you can explore the potential to rent a portion of your land or sell mineral rights or a timber deed to earn money to pay for your tiny home. TinyFest founder, Renee, and her husband Zev, are currently paying for their land through select harvest logging. This may sound intimidating, but you don’t have to be a logger with expensive equipment for this to be an option for you; You can sell a timber deed and have it paid at closing.

Financing Your Tiny Home - So Many Options

There are so many options for financing your tiny home dream. From tiny home builder and lenders to services specifically tailored towards tiny homes and ADUs, being a part of the TinyFest community offers the resources and community to solve every problem you may encounter through your journey.

To make it easier to understand the possibilities, we’ve created this quick comparison chart highlighting some of the most common financing options available.

Learn More at TinyFest

One of the biggest benefits of attending TinyFest is the chance to talk directly with builders, lenders, and industry experts who understand the unique challenges of financing small homes.

If you’re exploring the idea of building a tiny home or adding an ADU, learning about financing early can help you turn inspiration into a realistic plan.

TinyFest 2026 will be held at the Orange County Fair & Event Center in Costa Mesa, California on April 18 & 19, 2026. Get your tickets today!